Nigeria is a country that lacks political will to enforce laws unless it is self-serving (see this blog post on lack of political will here). The ongoing tax war between the federal government and Rivers State supports this claim. It is being touted that Lagos State is about to join the fray.

This article will attempt to dissect the issues involved, exploring the different elements at play, namely: background facts on the ongoing tax battle as we know it and the existing legal and policy framework on tax. These will inform the opinion on the veracity of the actions of the Rivers State government, as well as the concluding remarks. Let’s delve right into it.

What exactly is happening? Factual Matrix of the Ongoing Tax War.

This whole tax war is brought about as a result of a judgment of a Federal High Court sitting in Rivers State wherein that Court made a pronouncement that the collection of VAT in the State is the sole preserve of the Rivers State government. That the federal government could not therefore stop the Rivers State government from collecting VAT.

As a result of this pronouncement, the Rivers State Government immediately set about to enforce the judgment by tasking the Rivers States Revenue Service to commence collection of VAT from all bodies liable to pay VAT. In addition, the Rivers State House of Assembly has passed the Rivers State Value Added Tax No. 4, 2021 which effectively provides that the Rivers State government is to collect all VAT within its State.

Dissatisfied with the judgment, the tax collecting body of the federal government, the Federal Inland Revenue Service (FIRS), has noted an appeal to the Court of Appeal. It then applied to the Federal High Court for a stay of execution of its judgment. That application was refused, with the Federal High Court holding that to grant the application will be tantamount to murder and rendering its judgment ineffective.

The plot now thickens with the Lagos State government appearing to follow suit by currently pushing for the passing of its own VAT State Law. This law has now passed the first and second reading and according to Channels News report today, it has now passed into law although awaiting the Governor’s signature and assent. You can read all of these in this report by Vanguard.

Understanding the context of the ongoing war – the current allocation matrix by the Federal Government.

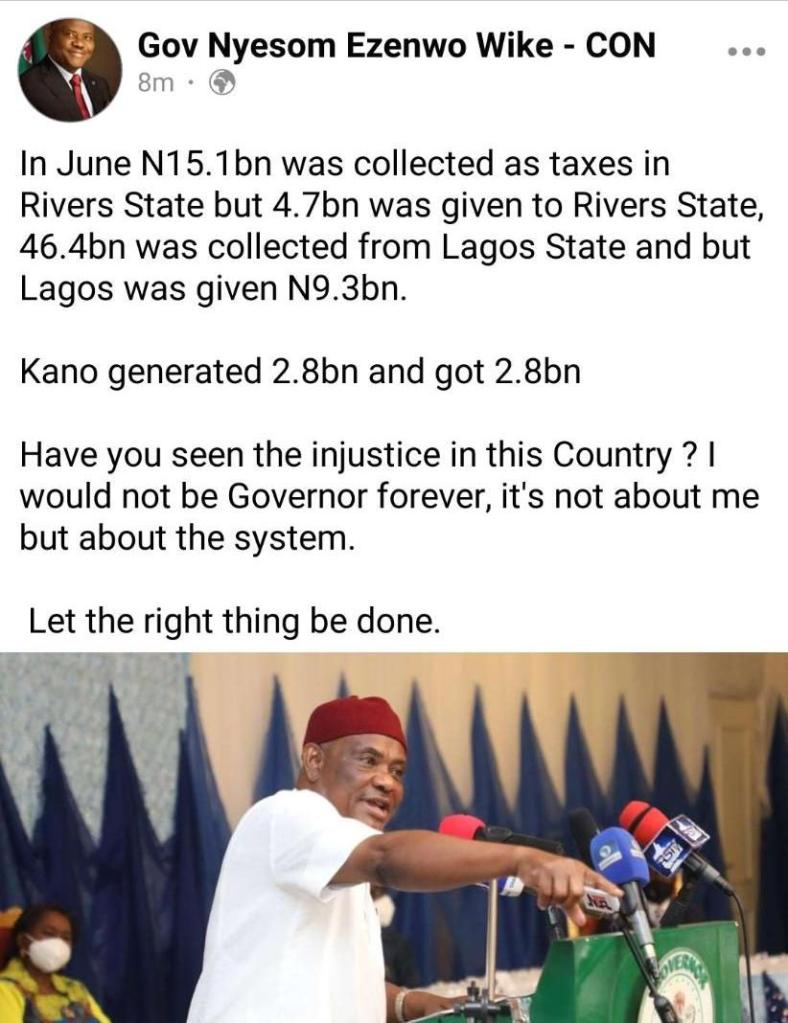

The whole debacle now playing out is a grievance on the allocation of revenue by the Federal Government. A look at the IG handle of the Rivers State Government shows a bleak and unfair picture of federal allocation of resources, if what the Governor says is anything to go by. A snapshot of this is attached below.

In essence, the Southern part of the country is denied more than 50% of the funds they generate internally from tax while their brethren in the North are not subjected to the same disadvantage. And thus, he says, this injustice cannot continue.

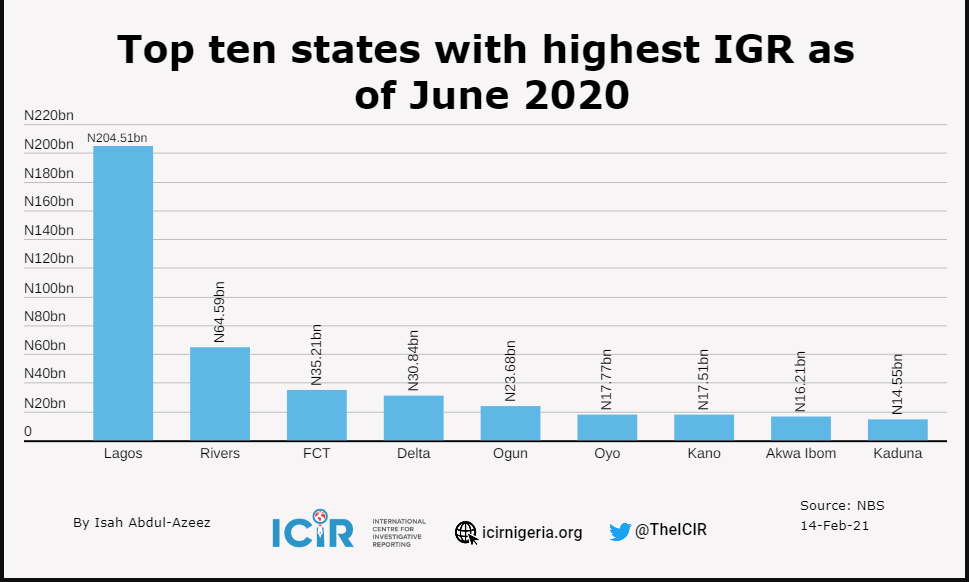

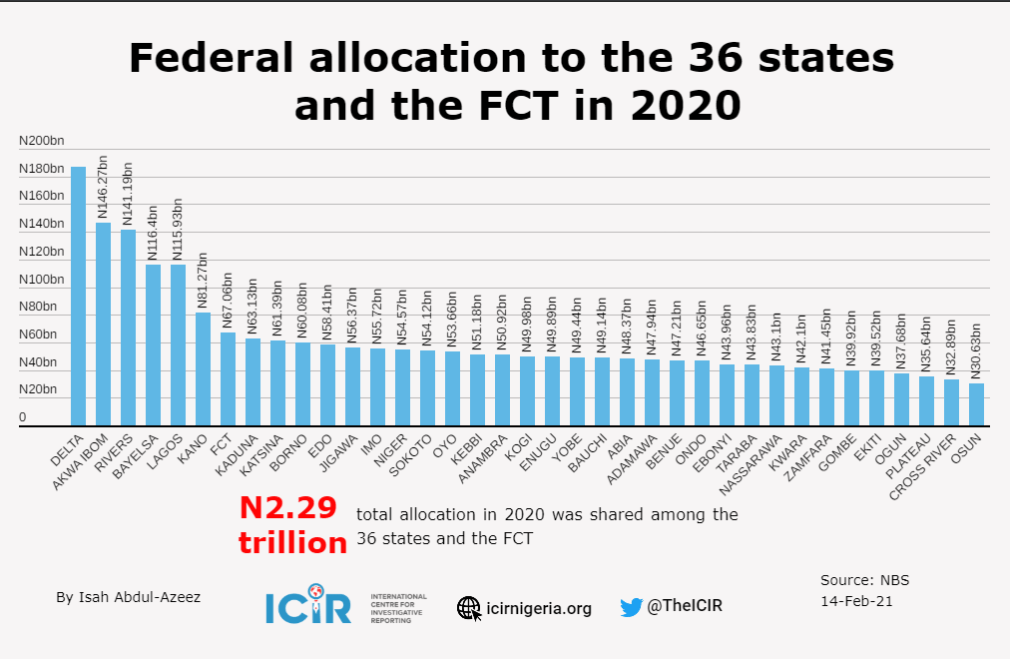

To perhaps point out though that a little reading from the International Centre for Investigative Reporting here revealed that Rivers State was among the 3 States that got the highest federal allocation in 2020, receiving N141.19BN of the N2.29 Trillion that was shared/allocated to all 36 States of the Federation. It should also be pointed out that Rivers State remained number 2 in the list of top 10 States with the highest IGR in Nigeria as of June 2020.

What is the position of the law? The Legal Framework on Tax in Nigeria.

As with everything in Nigeria, the starting point is the Constitution, as the grundnorm of the nation. The Constitution delineates law-making powers in the country, and by extension, the powers of the federal and states inter se. This it does by creating an Exclusive Legislative List and a Concurrent Legislative List in the Second Schedule to the Constitution.

The Exclusive Legislative List is the sole preserve of the Federal Government and no State is allowed to touch any of the matters set out on that list. The Concurrent Legislative List on the other hand levels the playing field and gives both the federal and state equal powers over all the subject matter that appears on that list, subject to the doctrine of covering the field. In this regard, section 4(7) of the Constitution provides that:

“The House of Assembly of a State shall have power to make laws for the peace, order, and good government of the State or any part thereof with respect to the following matters, that is to say –

(a) Any matter not included in the Exclusive Legislative List set out in Part 1 of the Second Schedule to this Constitution;

(b) Any matter included in the Concurrent Legislative List set out in the first column of Part II of the Second Schedule to this Constitution to the extent prescribed in the second column opposite thereto; and

(c) Any other matter with respect to which it is empowered to make laws in accordance with the provisions of this Constitution.

According to that Concurrent List, tax matters are also listed as falling within the equal competence of the federal and state. The relevant provisions are item 1 of the List. Due to its importance, it is reproduced in full hereunder:

“1. Subject to the provisions of this Constitution, the National Assembly may by an Act make provisions for –

(a) The division of public revenue

(i) Between the Federation and the States;

(ii) Among the States of the Federation;

(iii) Between the States and local government councils;

(iv) Among the local government councils in the States; and

(b) Grants or loans…(not applicable)

So, the question is whether the National Assembly has legislated over VAT in a way that precludes States from collecting VAT? Because if the National Assembly has, then the doctrine of covering the field precludes the States from legislating to go contrary to that federal law. Where however the federal law is silent on the matter, then this gives States the liberty to go ahead and legislate. What this also means inversely is that if the States beat the Federal Government to legislate on the matter, then the Federal Government cannot seek to undermine their laws by passing a later law to contradict the State law.

Has the National Assembly legislated on VAT? Yes, the National Assembly has. This is seen in the Value Added Tax Act of 2004. The VAT Act simply provides that the Federal Inland Revenue Service will be responsible for collecting VAT. It does not explicitly preclude States from having their own internal revenue service that deals with collection of VAT.

This of course begs the question whether properly interpreted, this provision precludes States from having their internal revenue service collect VAT and whether having a parallel VAT collection arrangement will in fact be prejudicial to economic growth and development especially for businesses. This will likely be the centerpiece of the appeal lodged by FIRS against the judgement of the Federal High Court in favor of the Rivers State government.

It is argued that going by the canon of interpretation that provisions that take away rights should be strictly construed in favour of preserving as much rights as possible, the only interpretation that would preserve the right of States to legislate under the Concurrent List is an interpretation that allows them to also collect VAT.

Otherwise, there was no point of putting it on the Concurrent List; it should have been made a subject matter for the Exclusive List. The Constitution understands that the centre cannot possibly be solely responsible for all revenue generation in the federation and that is why it decentralized this power to States as well.

What should perhaps be done is to clearly delineate how the collection by States and the Federal Government should be done in such a way as to prevent double taxation. And as well, a clear formula for division of the collected taxes between the federal and state that is fair and transparent should be adopted.

(Interested in reading about the VAT generally? Check out this article here seen on Mondaq. And for a good summary of other types of taxes, check out this article here).

What is the right thing to happen? Proposed tax policies and how it helps the country.

Tax remains a vital source of revenue generation for any economy. With a pandemic like COVID-19 for instance, we now know that it is all the more important for countries to be self-sustaining and generating their own income rather than waiting for grants for instance and foreign donations.

In a country like Nigeria where States are responsible for their affairs, they should not be hamstrung in the way they generate their revenue. And arguably this is the reason why the Constitution puts the issue of revenue generation on the concurrent legislative list. States should be allowed to control their taxes subject of course to the principle that they must be held to account for how they spend the revenue generated from all sources inclusive of tax.

Closing Thoughts.

Ultimately what is taking place now is what ought to have long taken place if our leaders are indeed not self-serving and selfish. The Constitution has been with us since 1999, which is a period of more than 20 years. Why were these provisions not enforced this whole time one might ask?

Yes, while the current efforts of the Rivers State Governor to want to put things right is commendable, it cannot be helped but noticed that this has only come to the fore because it is self-serving. It may look egalitarian and selfless at first blush, but let’s face it, it is not. The only reason why this has suddenly become an issue is because the ones complaining feel that they are no longer getting their fair share of the cake. The question remains, do we really see the results of all these billions collected in tax in the infrastructure and quality of living in Nigeria? We all know the answer to that question.

So, where do all these monies go to? Are they being funneled elsewhere? Is this a case of using State machinery to fight personal wars of self-preservation? While the move to uphold the laws as they exist as regards VAT is laudable, the excitement is half-hearted because the results of all the monies generated from tax in the quality of life of the average Nigerian and the general conditions of living in Nigeria is hard to see.

Perhaps to examine the said Rivers State more closely. The State Government still owes primary and secondary school teachers their wages since 2016 and is not making any moves to pay them, despite their protests earlier this year – see this news report. And yet very ironically, the same government donated 500Million to another State instead of solving the problems in his house.

Pensioners are still owed; according to one report, they are owed for 9 years outstanding pension (see here). General unemployment rate in the State remains at an all-time high, an average of 29.6% according to this statistic seen here. According to the State of States Report from BudgIT seen here (at p.103), “1.71m people of Rivers state’s 3.92m labour force are unemployed—the third highest in the country while 775, 974 residents remain underemployed”. Basic education is still not free.

All these issues fester and Rivers State’s internally generated revenue in 2020 alone is N92,986,084,316.65 and N144,065,442,569.00 in 2021. These figures can be seen in the Rivers State 2020 Budget here.

A close look at this budget at page 35 which shows the capital expenditure summary reveals an unsettling allocation of funds that reveals a misplacement of priorities with respect. According to the aforementioned State of States Report for instance, “the Education and Health sector got only 7.12bn and N4.2bn for capital expenditures respectively in 2019 while N35.8bn was spent on Security/Contingency and another N19.2bn on Government House capital expenses in the same year.”

It is unclear why law makers for instance are receiving a dizzying N3,704,000,000.00 and there is widespread hunger in the State. Should leaders be receiving such exorbitant amounts when the people they serve are hungry?

The office of the Deputy Governor for example is given N140,000,000.00 for 2020 (at p.30) which translates to 11.6Million in a month for one public office in a State where that amount can feed more people and send them to school. Nigeria is one of the few places in the world where public servants such as those in the helm of affairs use public office to enrich themselves instead of equitably distributing the resources meant for everyone in the country.

Yes, States should be left to collect their taxes because that is what should happen in a truly federal set-up. There should be equality as regards taxes and this is what the Constitution itself envisages in making tax a matter on the Concurrent Legislative List. But at the end of the day, the States must be held to account for how they spend these monies they want to now be collecting. Looking at the state of affairs of teachers and pensioners in Rivers State, this becomes all the more important.

In enacting the Rivers State Value Added Tax No. 4, 2021, the Rivers State government is well within its constitutional rights to enact on the matter. It is however hoped that this will translate into improving the the lives of all persons living in Rivers State.

© Glory Ifezue Foundation, 2024.

{kind=link}

Leave a comment